November 2024 New Residential Construction

What happened

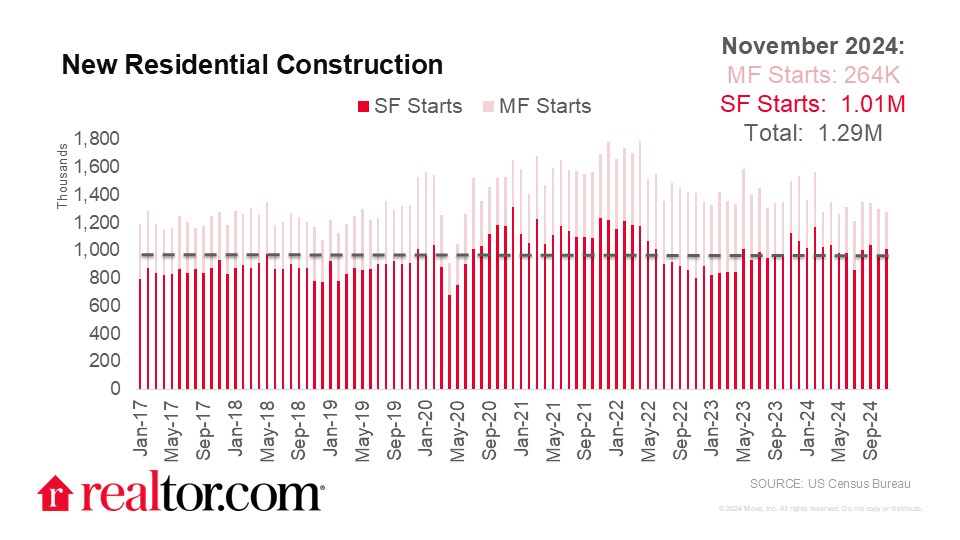

New residential construction activity slowed in terms of starts and completions for the third consecutive month in November, but permits issued for new projects picked up slightly. The number of units permitted for construction rose to 1,505,000, an increase of 6.1% over October 2024 and back to almost exactly the same level as in November 2023. Though builders appear confident enough about the future to keep permitting at its same high level, their short-term decisions about new home starts and completions reflect more trepidation. The number of housing units started in November fell to 1,289,000, a 1.8% retreat from October and a 14.6% reduction from November last year. Completions dipped as well month-over-month, falling 1.9% from October’s level to 1,601,000, but this still marks a 9.2% improvement over November 2023. The relative softness of the multifamily segment is most pronounced in starts, where the number of units started in buildings of five or more units dropped 24.1% month-over-month and 28.8% year-over-year. These multifamily units make up just 20.5% of all units started, compared to 32.0% of permitted units and 34.0% of completed units. Expect the number of completed units in buildings of five or more units, which dropped 11.1% from October but is still up 13.6% from last November, to slide in the coming months and years as a result of the weakness in multifamily starts.

Where it happened

Bucking the national trend completely is the region with the least overall new construction activity, the Northeast. Northeastern units permitted for construction are 36.2% higher than they were last year, with all of that growth coming from multifamily projects as single-family permits remained flat year-over-year. Northeastern completions were noteworthy as well, nearly doubling the overall figure from November 2023 despite single-family completions being down 7.3% year-over-year. This data is a bit noisy because of the smaller sample sizes, but it still gives credence to the strength of the multifamily segment in the Northeast compared to the rest of the country. Meanwhile the region that has been the main focus of new construction activity in recent years, the South, saw year-over-year reductions in overall permits (-0.6%), starts (-11.1%), and completions (-0.9%). While Southern single-family projects lead the way in terms of starts (-1.6% year-over-year) and completions (+0.7% year-over-year), they (-3.9% year-over-year) actually drag down the permitting growth number. New construction activity is holding basically steady in the South, if tapering down a bit while other regions start to step into the spotlight.

What does this mean for homebuyers, sellers, homeowners, and the housing market

It’s unsurprising to see a bit of hesitation around starting new construction projects in the current landscape, especially the sharp slowdown in starting projects with five or more units. The median asking rent nationwide has fallen year-over-year for sixteen consecutive months, so return on investment for building large rental communities continues to look less attractive. The inventory of homes for sale was up 26.2% year-over-year in November and has reached at least 95% of its pre-pandemic level in the South and West, so competition for newly-built homes going onto the market is strong. Mortgage rates, which have been a headwind to the housing market for years at this point, have finally started to relent after increasing every week through October. Their effect of slowing down prospective homebuyers can still be felt as builders pulled back on starting and finishing projects this month, but optimism about them falling is a driver of increased permits.