Freddie Mac Mortgage Rates—Sept. 26, 2024

What happened to mortgage rates this week

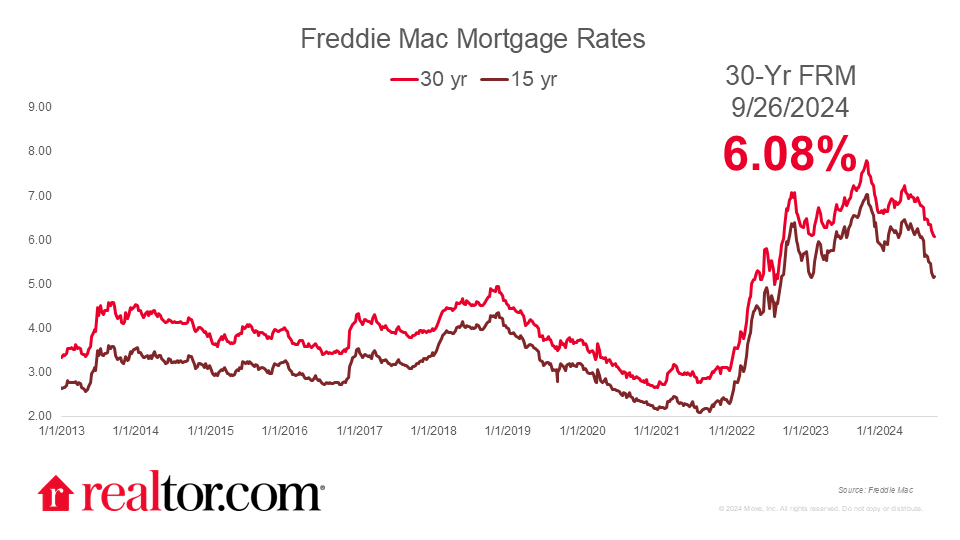

The Freddie Mac rate for a 30-year mortgage fell slightly by 1 basis point to 6.08% this week, reaching its lowest level in two years. After nearly a year of speculation about when rate cuts would start, recent signs of softer inflation and a cooling labor market have given the Fed the confidence to begin normalizing policy. Longer-term interest rates have already started reflecting this shift, with the 10-year yield down to 3.8% from its calendar-year high of 4.7% in April and slightly more from the 16-year high of 5.0% reached in October 2023. Similarly, mortgage rates have dropped a full percentage point from their May 2024 peak of 7.2%, and are now more than a point and a half below the 7.8% high reached in October 2023—a 23-year record.

What it means for the housing market

Looking ahead, with the Fed’s expected rate cut now in place and markets having largely priced in such changes, we don’t expect a significant drop in rates moving forward. Mortgage rates are likely to stabilize in the 6%–6.2% range through the rest of the year, potentially dipping into the high 5% range by next spring.

With mortgage rates dropping, prices declining, inventory increasing, and homes staying on the market longer, a sense of optimism is emerging this fall. However, as mortgage rates trend downward, a key question for home buyers is whether to keep waiting or move forward with their purchase. As we don’t expect significant rate improvement before the end of 2024, for buyers looking to close on a home before the year’s end, taking advantage of the upcoming “Best Time to Buy” could be a smart choice. This period offers a favorable mix of market conditions more advantageous to buyers compared to the rest of the year. For those who want to wait longer for lower mortgage rates, it is important to think through the tradeoffs of buying in a typical busier spring season. For example, while mortgage rates are expected to flow lower, home price growth may pick up again by spring, particularly if the historically slow-to-recover inventory remains tight.