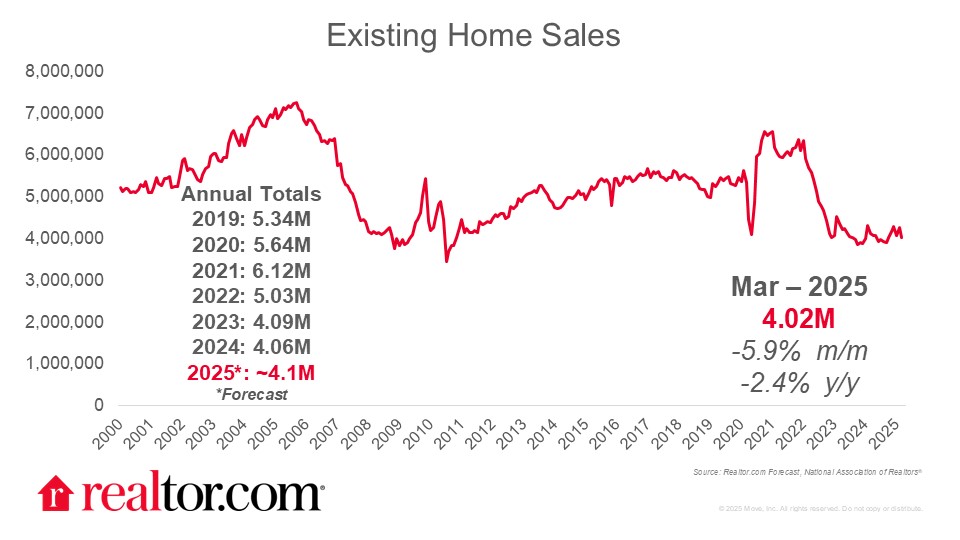

March 2025 existing-home sales

softened in March 2025, dropping 5.9% from February to a pace of 4.02 million. Sales also trailed 2.4% behind the pace one year ago. Pending home sales picked up in February, but remained lower than one year ago, a trend that continued in the March Realtor.com pending data, suggesting more softness ahead.

These March home sales would likely have gone under contract in February and early March, when mortgage rates declined from near 7% to 6.6%. The tailwind of falling mortgage rates, however, was likely offset by rising concerns about the outlook for personal financial situations and job security reported in consumer surveys, despite the fact that actual labor market data .

Home prices continue to climb, but growth rate slows

The median home sales price continued to grow, registering $403,700. However, the rate of growth ebbed to 2.7% in March from 3% to 4% in prior months. Meanwhile, inventory climbed 19.8%, to 1.33 million, pushing months supply from 3.5 to 4, a figure consistent with a balanced market.

What this data means for what’s ahead this year

We’ve just passed the Best Time To Sell (April 13–19), and now, we’re moving into the heart of home sales season when more homeowners list their homes for sale. While the first quarter typically accounts for roughly a fifth of the year’s home sales, the next five months usually make up nearly half of the year’s existing-home sales. Year to date, home sales trail what we saw in 2024 by roughly half a percentage point, when adjusted for seasonality. To see the modest annual growth anticipated in the Realtor.com 2025 Housing Forecast, we need to see sales growth in these busy months.

Home sellers are optimistic, but buyers?

Recent data shows that sellers continue to be optimistic. New and active listings increased compared with the prior year, and a recent Realtor.com survey found that 81% of potential sellers think they will get their asking price or more this year. The key question for this year’s buying season is whether homebuyers will have their currently shaky confidence restored soon enough to sync with the key buying season. The past few years have hinged on whether there would be enough sellers, but as the proverbial housing shelves are better stocked, 2025 is more likely to be about where there are buyers.

Regional trends show that affordability matters

Sales were lower than February in all four regions, with the smallest declines in the Northeast and Midwest, where hallmarks of market competitiveness (e.g., down payments and market hotness) show that affordability has kept buyers relatively more active. Looking ahead, however, the South and West have been the regional leaders on adding more housing supply, according to Realtor.com research. That is likely to improve affordability in these regions. In fact, the Northeast (+7.7%) and Midwest (+3.5%) saw the highest median home sales price growth, while the West (+2.6%) and South (+0.6%) saw more modest increases in March.